US interest rates go up, but the UK bides its time

10th April 2017

The US central bank, the Federal Reserve, has increased interest rates for a third time.

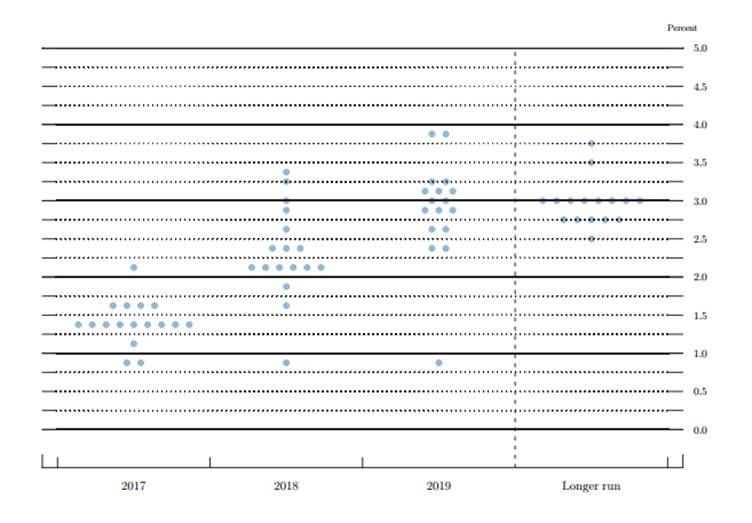

This might look like a piece of modern art, but it’s not. The illustration above is what has become known as the “dot plot”. Each dot represents where a member of the US Federal Reserve’s rate-setting committee expects short term interest rates to be at the end of the year. For example, the longest line of dots in 2017 shows that nine members expect an end of year rate of around 1.35%, while the most popular ‘longer run’ estimate is 3.0%.

In March the Federal Reserve raised its main interest rate by a well-publicised 0.25% to a band between 0.75% and 1.00%. The general view now is that 2017 will see two more increases – hence the 1.35% (actually 1.375%) line on the dot plot.

The day after the US central bank raised its rates, the Bank of England’s Monetary Policy Committee (MPC) voted 8-1 in favour on holding base rate at 0.25%. The sole dissenter, Kristin Forbes, wanted a 0.25% rate rise, but her voice will soon disappear as she leaves the MPC in June. According to the Financial Times, traders do not see the first UK rate rise happening until early 2019. The Bank is expected to ‘look through’ (that is, ignore) the rise in inflation that will occur in 2017 as the weak pound works its way through to retail prices. The latest inflation data, showing a 0.5% jump in the CPI annual rate to 2.3% for February, underlines the point.

It is now over eight years since the Bank cut rates to a fraction of 1%. The impact of such a long period of ultra-low rates has been controversial, particularly its effect on savers with cash deposits and final salary pension schemes with burgeoning liabilities.

If you need income from your capital, there are plenty of options to consider that offer more than deposit rates. For example, the average dividend yield on UK shares is around 3.5%. For more details on the income options available, do talk to us.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.