Marmite pricing: the bad news

2nd November 2016

Inflation rose to 1% in September, but that will not be the end of the story.

Last month a spat between Tesco and Unilever over the pricing of products under a new contract saw Marmite temporarily removed from the shelves of Tesco’s internet shopping website. The two parties resolved the issue quickly once it hit the headlines, but it was a reminder that the plight of the pound since the Brexit vote will inevitably translate into price increases.

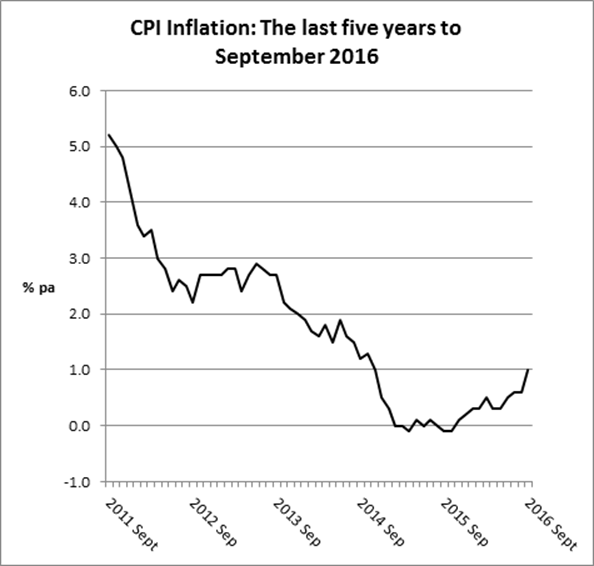

The latest inflation data from National Statistics (NS) also showed a rise in inflation, up from 0.6% in August to 1.0% in September. As the graph shows, there has been a marked rise in the Consumer Prices Index (CPI) since the negative numbers recorded in 2015.

NS says that September’s inflation spike was not a reflection of sterling’s recent weakness, pointing out that “there are reports of businesses having measures in place to protect against exchange rate changes in the short-term.” The NS view is supported by the fact that the price of goods (largely imported) is still showing a year-on-year drop, while it is services (mainly UK supplied) where inflation is visible. However, it seems certain – as the Marmite issue showed – that goods inflation will start to emerge soon. Some economists are suggesting we could see 3% inflation in 2017, well above the Bank of England’s central 2% target.

The likely return of inflation is a reminder of an investment risk which had seemingly disappeared in recent years. Even though interest rates have been extremely low (and moving lower), while inflation was quiescent, the purchasing power of deposits was hardly being eroded. That is now starting to change, with little likelihood that the Bank of England will push up interest rates amidst the current Brexit-driven economic uncertainties.

If you have cash on deposit beyond your rainy-day needs, the return of the oft-slayed, never-killed inflationary dragon should make you consider other options for your money.

The value of your investment can do down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.