At least we beat Mexico

1st December 2013

The UK state pension system has come under the spotlight again.

The Organisation for Economic Cooperation and Development (OECD) has just published its 2013 snapshot of pension provision amongst its members. As usual, it does not paint a great picture for the UK:

- Based on the existing UK state pension structure (basic state pension and state second pension), someone on full time average earnings (£35,900 according to the OECD) with a complete working life can expect the state pensions to equal 32.6% of their earnings on retirement. In the OECD league table that puts the UK one from bottom, with only Mexico (28.5%) scoring less. The OECD average is 55.4%.

Higher earners (150% of average earnings in OECD-speak) can expect 22.5% replacement retirement income compared to the OECD average of 48.4%.

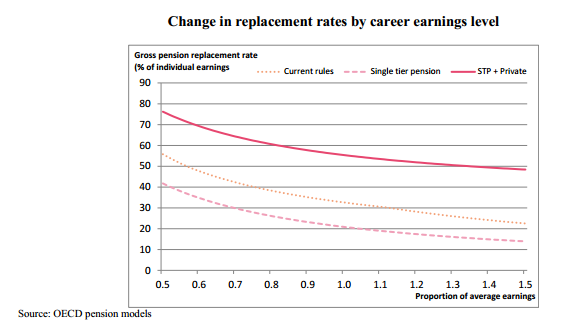

- When the OECD looks at the new single tier pension due in 2016, its conclusion is that the replacement rate would fall to just 21%. The drop is a reminder that the new regime will mean the loss of the earnings–related element provided by state second pension.

- The situation is somewhat redeemed when the OECD adds into their calculations an 8% contribution assumption under pension auto-enrolment, even though this is not compulsory. The pension that auto-enrolment produces, when combined with the single tier pension, brings long term UK benefits in line with the OECD average at all earnings levels, as the graph below shows. Nevertheless, the high earner still faces a replacement rate of slightly under half, with a pension age of at least 67 from 2028.

The main upside from joining Mexico in the relegation zone is UK state retirement provision is relatively cheap. The OECD says it currently costs 6.2% of GDP against an average of 7.8% and, for example, 13.7% in France.