A £50,000 higher rate tax threshold?

1st November 2014

Mr Cameron’s promise of a £50,000 starting point for higher rate tax is not all that it seems.

The Prime Minister ended the Conservative Party Conference with a pledge to increase the higher rate threshold – the starting level of income at which 40% tax is payable – to £50,000 “in the next Parliament”. At present, the threshold is £41,865 (made up of a £10,000 personal allowance plus a £31,865 basic rate band). Although it sounded generous, the reality was rather different:

- “In the next Parliament” could mean in 2020/21, as governments now have fixed five year terms and the next one does not start work until 2015/16.

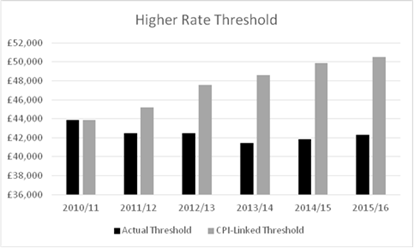

- The 2015/16 threshold has already been set at £42,285 – a 1% increase over this year’s level.

- A rise from £42,285 in 2015/16 to £50,000 in 2020/21 would be equivalent to annual increases of 3.4%, which sounds rather less impressive, especially if you consider that 2% of that is the expected inflation rate.

- The threshold at the start of the current Parliament in 2010/11 was £43,875, unchanged from the previous tax year.

- Had the 2010/11 threshold figure been increased in line with inflation, as measured by the Consumer Price Index, it would be over £50,500 next tax year, as the graph below shows.

- For most earners the benefit of the increased threshold would be offset by a corresponding increase in the limit for full rate National Insurance Contributions (NICs), which currently matches the higher rate threshold. Thus, if you are an employee, you would save 20% in tax, but then pay an extra 10% in NICs.

As ever, waiting for politicians to reduce your tax bill will probably prove less reliable than making sure your own personal tax planning is up to scratch.

Tax laws can change. The Financial Conduct Authority does not regulate tax advice.